Accumulator, decumulator, target, pivot are all structured products based on complex derivatives. This post is explaining how they work and what are their expected profit & loss profiles.

ACCUMULATOR

DECUMULATOR

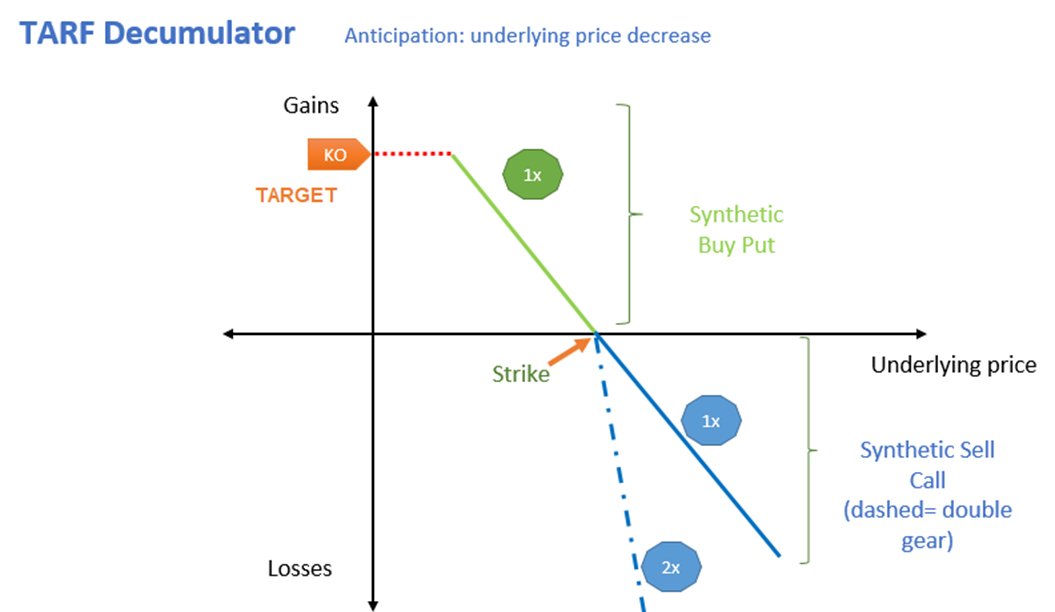

TARGET REDEMPTION FORWARD ACCUMULATOR

TARGET REDEMPTION FORWARD DECUMULATOR

TARGET REDEMPTION FORWARD ACCUMULATOR with double gear & Kick In barrier

PIVOT TARGET REDEMPTION FORWARD (with double gear)

PIVOT TARGET REDEMPTION FORWARD (with double gear) + Kick In barrier

An accumulator is an option based structured product for investors who hold a positive view of an underlying equity price or currency 1 relative to currency 2 FX rate.

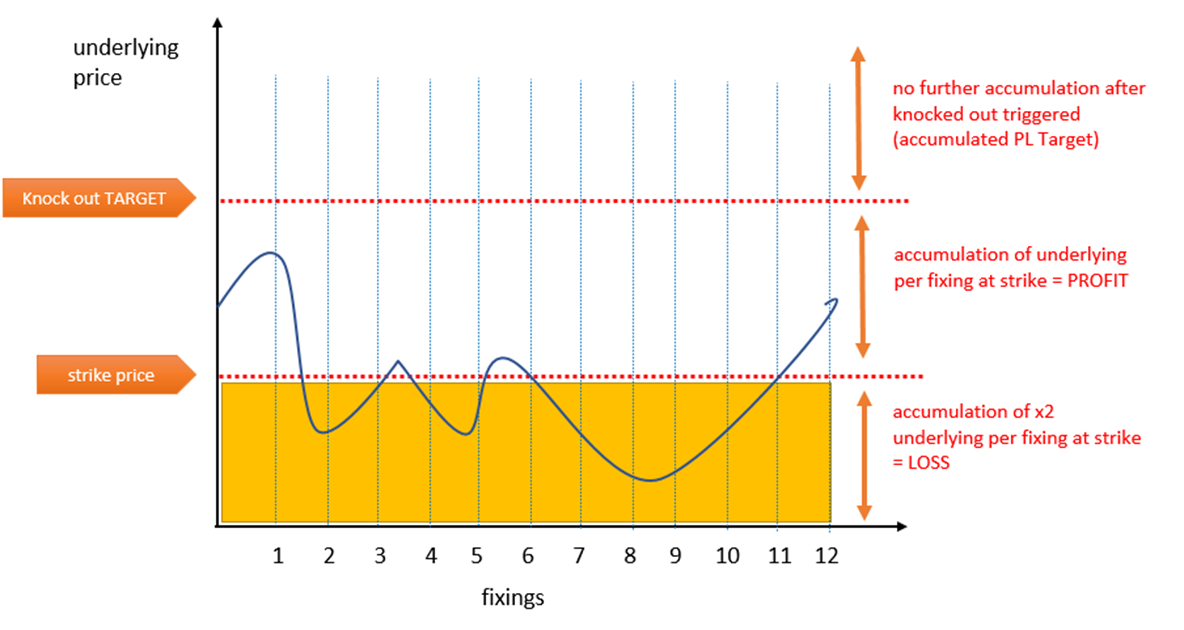

Investors is binding to accumulate (buy) over scheduled periods a determined amount of underlying (equity or currency 1) at the strike rate till expiry or early termination date.

The contract terminates early [i.e. knocks out] when the underlying breaches pre-specified high barrier.

Some accumulator contracts include a gear condition (multiplier), under which investors have to accumulate certain multiples (e.g. 2x) of the stated number of the underlying when the spot price falls below the strike price

Some may also include a number of guaranteed periods (also refering to “minimum accumulation amount”) when the KO price is not triggered despite the spot price jumps above it. There’s no gearing for guaranteed periods.

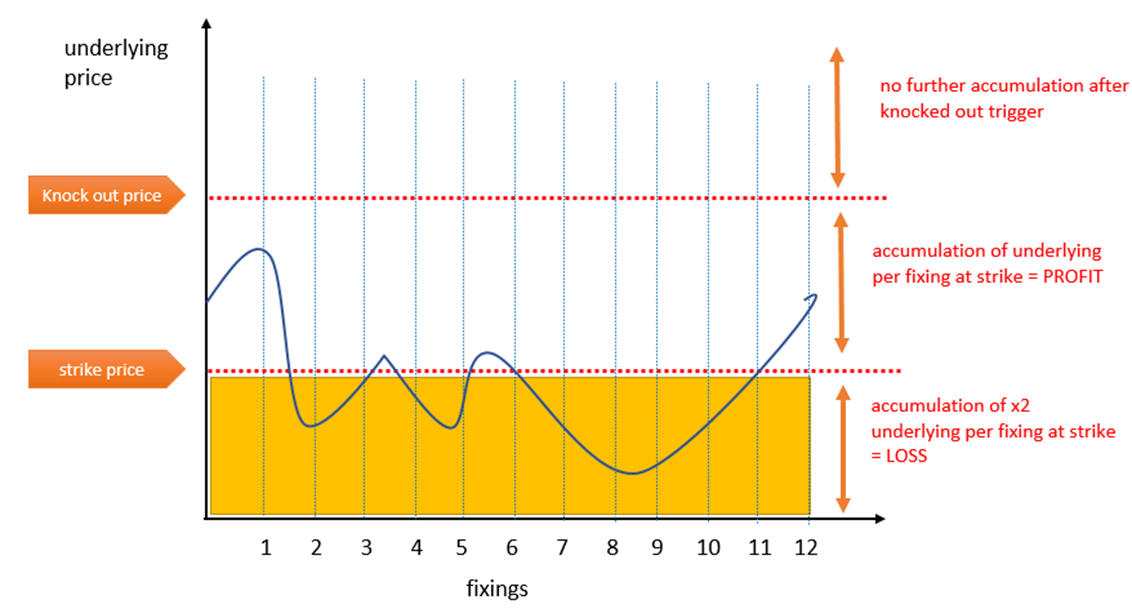

Scenarios:

1 fixing spot price > strike => investor is cumulating a profit

2 fixing spot price < strike => investor is cumulating a loss, potentially by buying x2 underlying nominal (when multiplier)

3 fixing spot price > high barrier => contract terminates after potential guaranteed periods

Scenarios Diagram

P&L Diagram

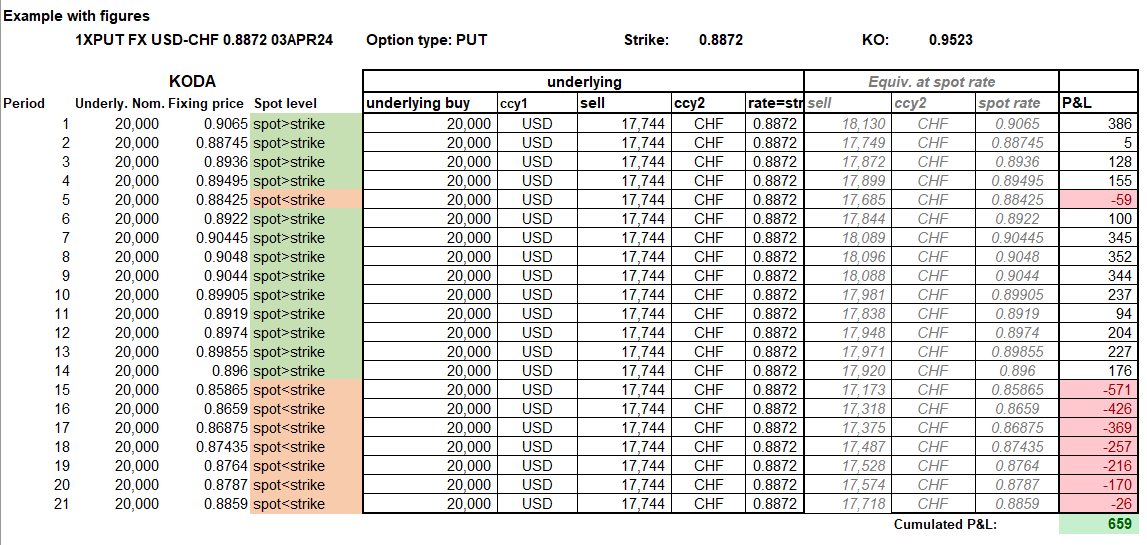

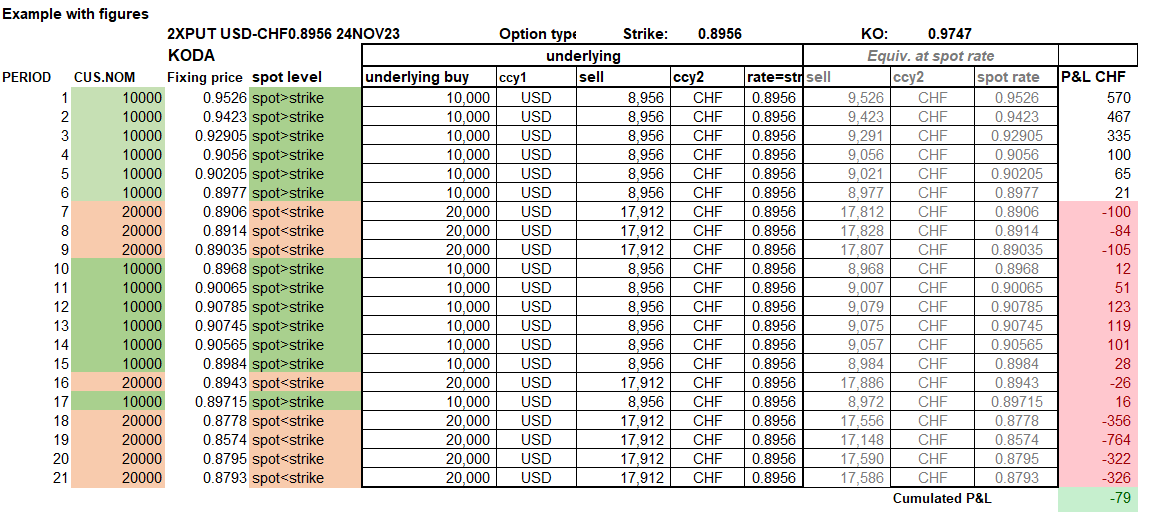

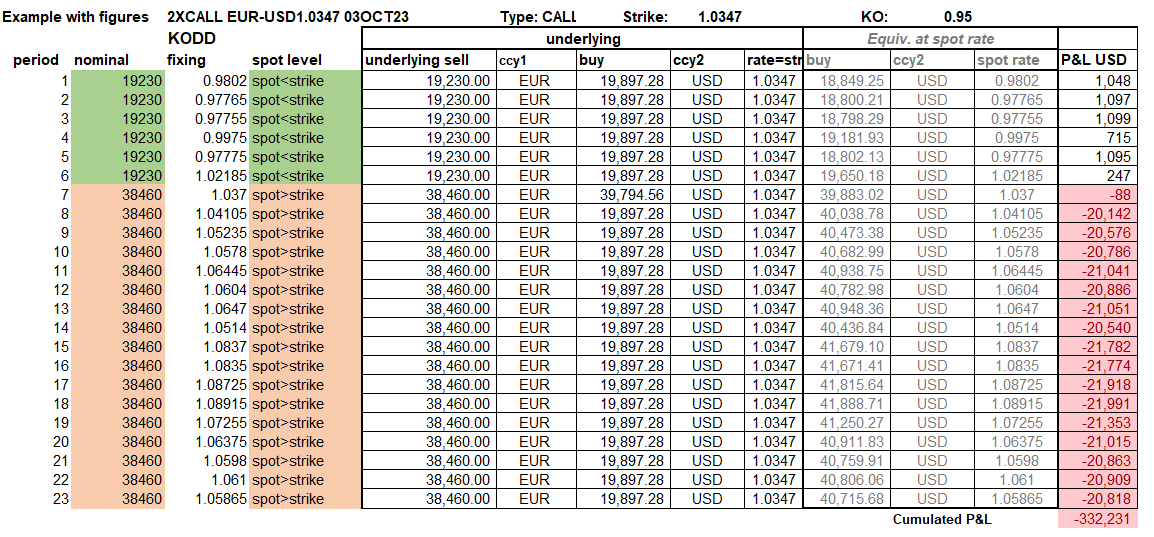

Example with figures:

ACCUMULATOR (with double gear)

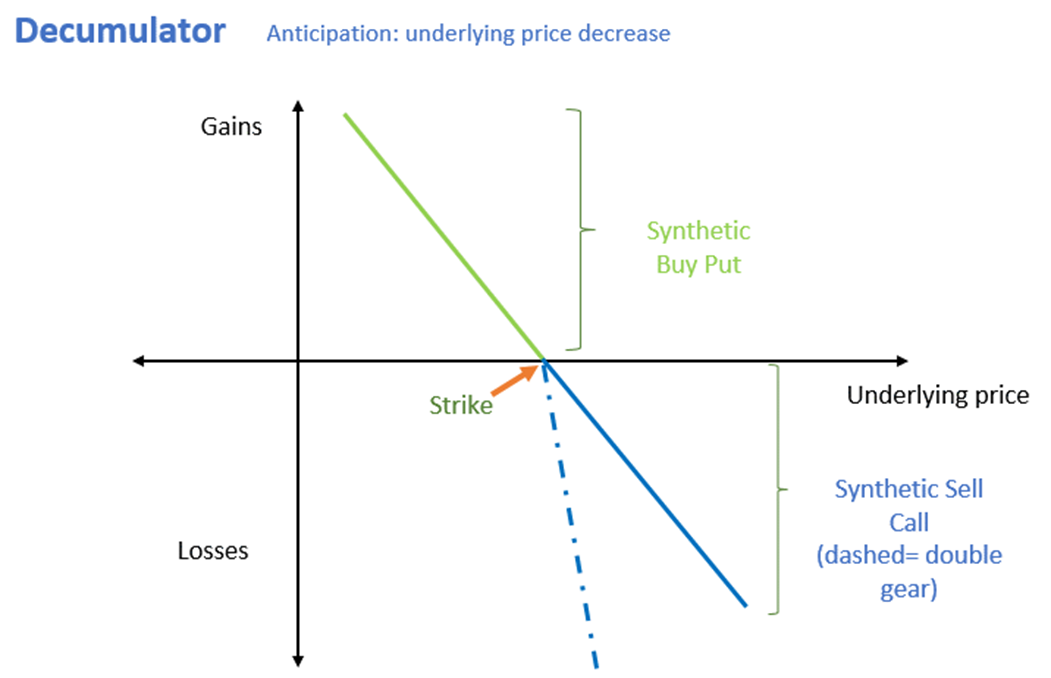

Conversely, a decumulator is an option based structured product for investors who hold a negative view of an underlying equity price or currency 1 relative to currency 2 FX rate.

Investors is binding to decumulate (sell) over scheduled periods a determined amount of underlying (equity or currency 1) at the strike rate till expiry or early termination date.

The contract terminates early [i.e. knocks out] when the underlying breaches pre-specified low barrier.

Some decumulator contracts include a gear condition (multiplier), under which investors have to sell a certain multiples (e.g. 2x) of the stated number of the underlying when the spot price falls below the strike price

Some may also include a number of guaranteed periods (also refering to “minimum decumulation amount”) when the KO price is not triggered despite the spot price falls below it. There’s no gearing for guaranteed periods.

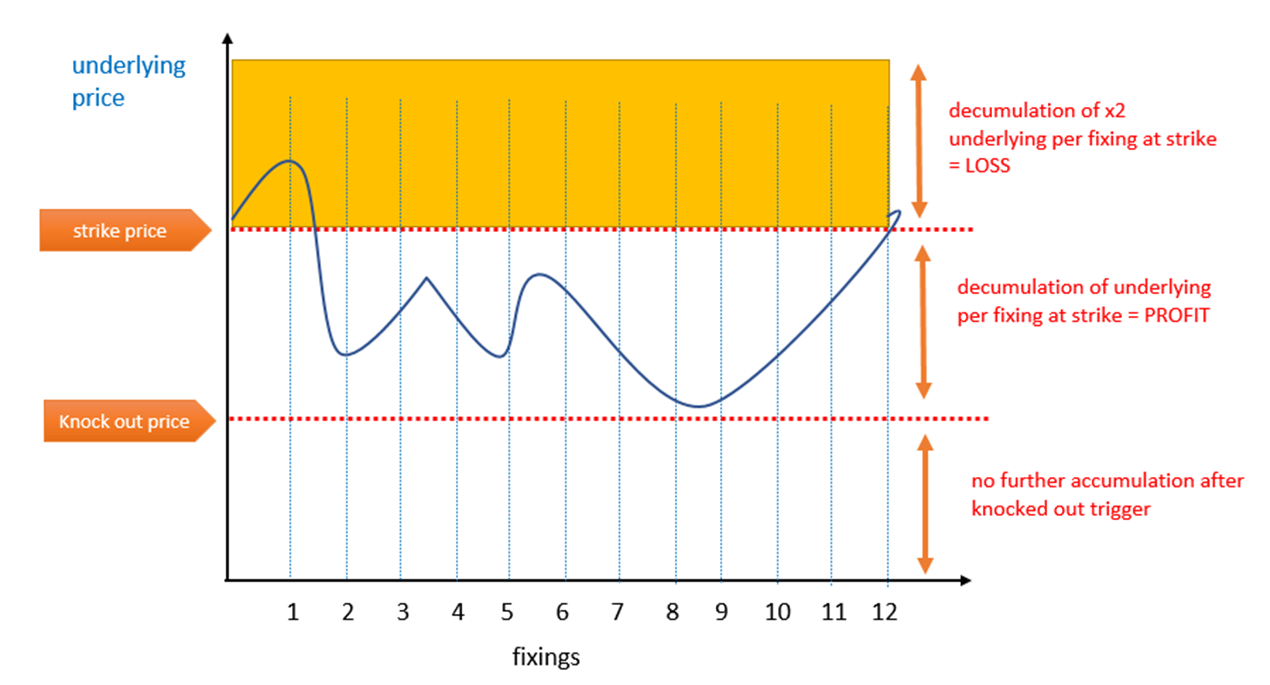

Scenarios:

1 fixing spot price < strike => investor is cumulating a profit

2 fixing spot price > strike => investor is cumulating a loss, potentially by buying x2 underlying nominal

3 fixing spot price < low barrier => contract terminates after potential guaranteed periods

Scenarios Diagram:

P&L Diagram:

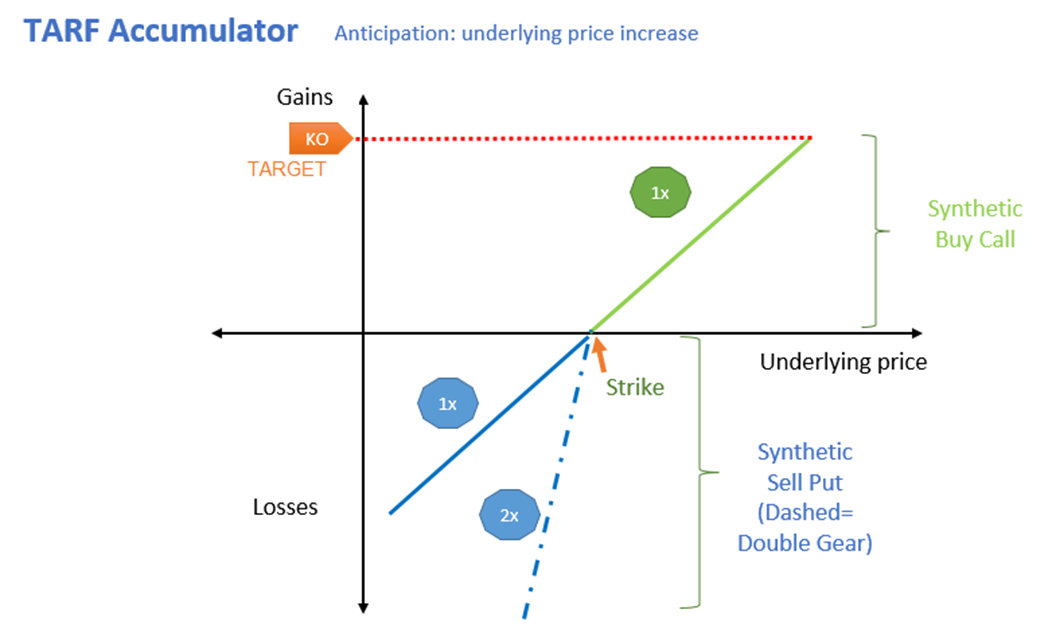

FX TARGET REDEMPTION FORWARD ACCUMULATOR

With “Put” option type, a target redemption forward accumulator is basically same as a “vanilla” accumulator, but including a cumulative gain cap involving an early knock-out when reached.

Investors is binding to accumulate (buy) over scheduled periods a determined amount of the selected underlying currency 1 at the strike rate till expiry or early termination date.

The contract terminates early [i.e. knocks out] when the cumulated P&L is reaching a pre-determined level, namely the “Target”.

Some accumulator contracts include a gear condition (multiplier), under which investors have to accumulate certain multiples (e.g. 2x) of the stated number of the underlying when the spot price falls below the strike price.

Scenarios:

1 fixing spot price > strike => investor is cumulating a profit

2 fixing spot price < strike => investor is cumulating a loss, potentially by buying x2 underlying nominal

3 cumulated P&L > Target => contract terminates when target is reached

Scenarios Diagram:

P&L Diagram:

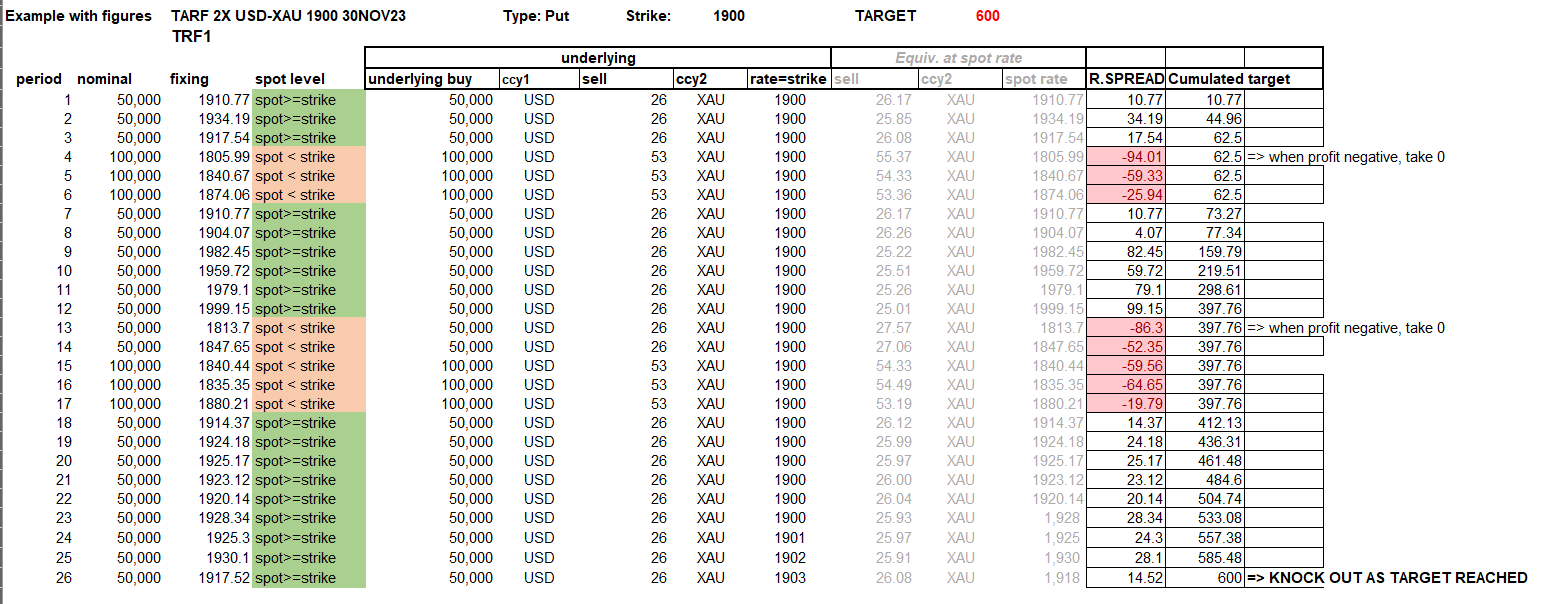

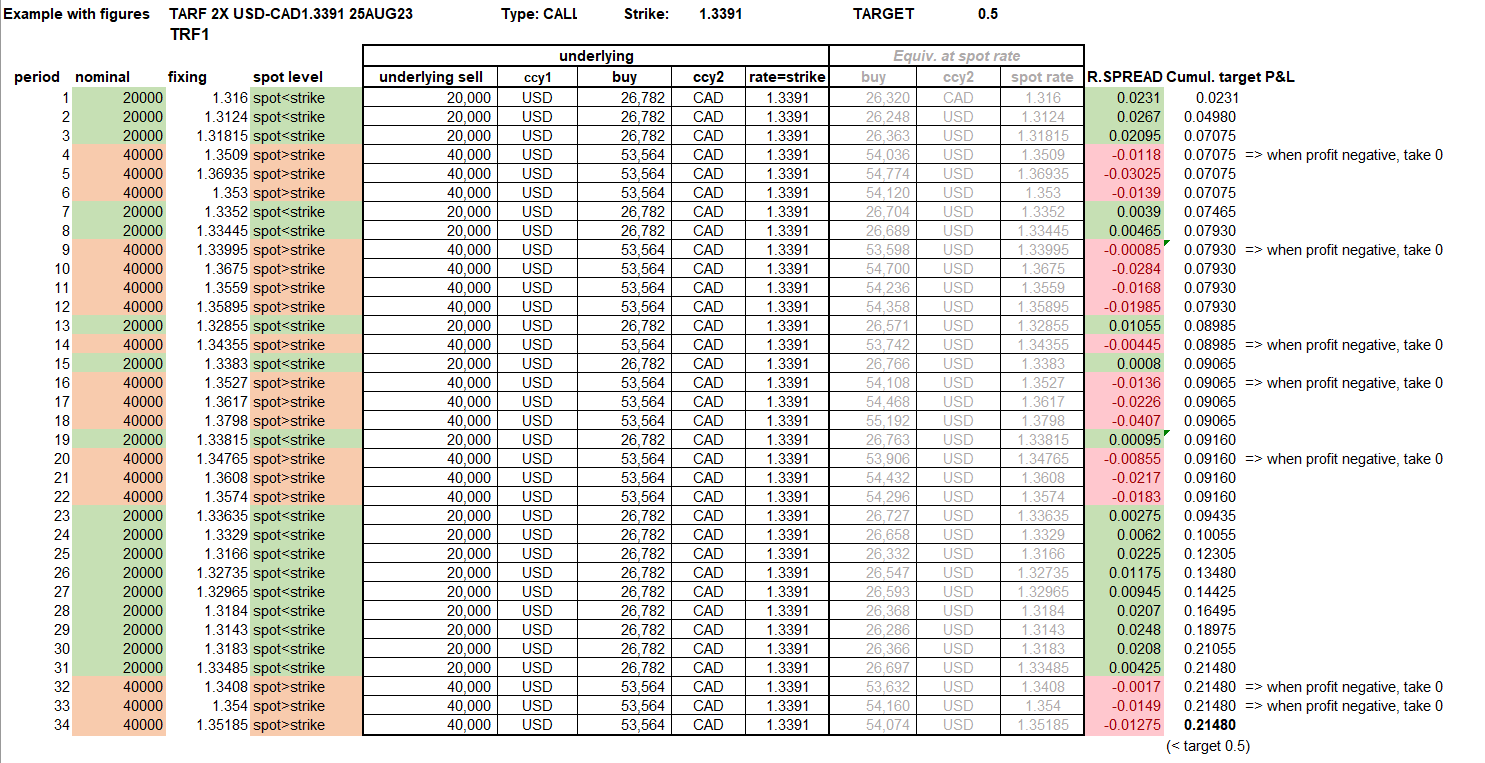

FX TARGET REDEMPTION FORWARD DECUMULATOR

With “Call” option type, a target redemption forward decumulator is basically same as a “vanilla” decumulator, but including a cumulative gain cap involving an early knock-out when reached.

Investors is binding to decumulate (sell) over scheduled periods a determined amount of the selected underlying currency 1 at the strike rate till expiry or early termination date.

The contract terminates early [i.e. knocks out] when the cumulated P&L is reaching a pre-determined level, namely the “Target”.

Some decumulator contracts include a gear condition (multiplier), under which investors have to sell a certain multiples (e.g. 2x) of the stated number of the underlying when the spot price falls below the strike price.

Scenarios:

1 fixing spot price < strike => investor is cumulating a profit

2 fixing spot price > strike => investor is cumulating a loss, potentially by buying x2 underlying nominal

3 cumulated P&L >= Target => contract terminates when target is reached

Scenarios Diagram:

P&L Diagram:

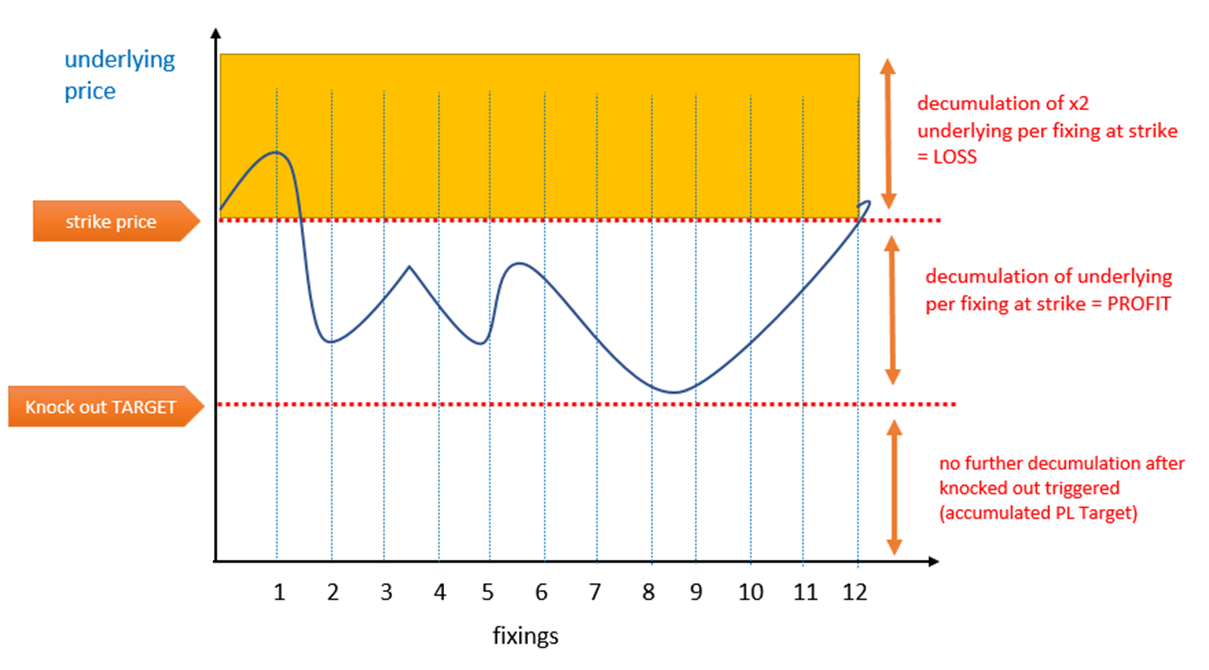

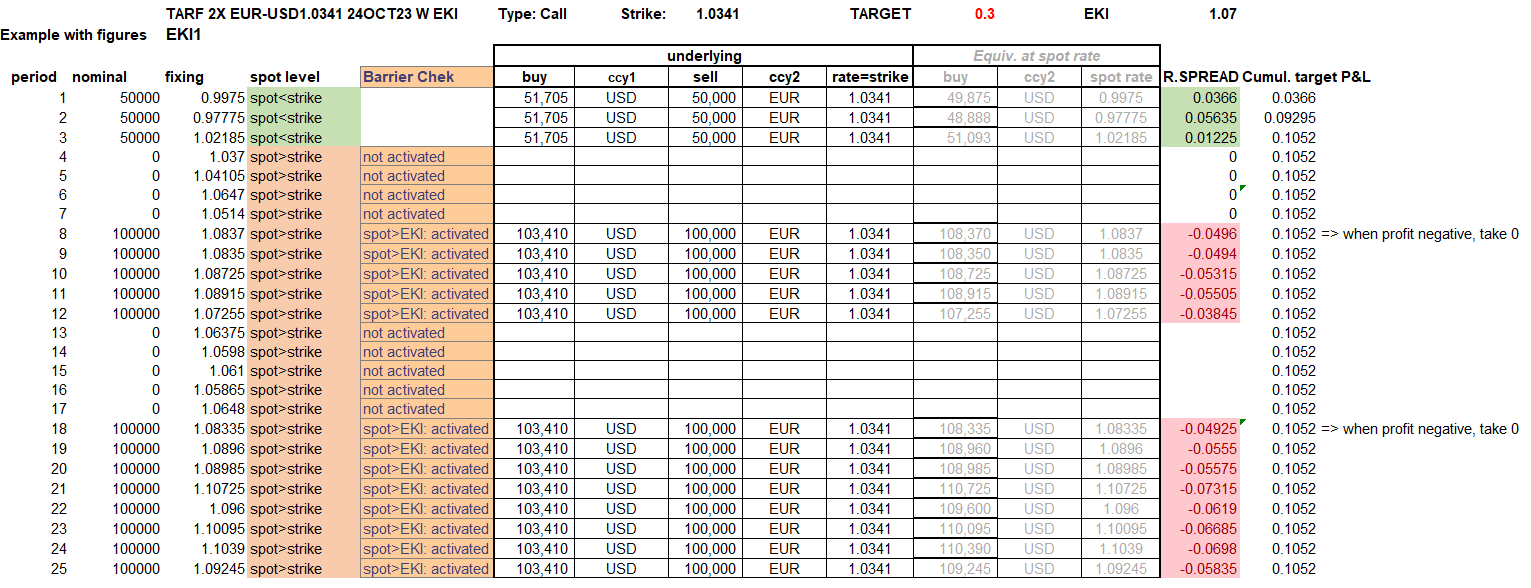

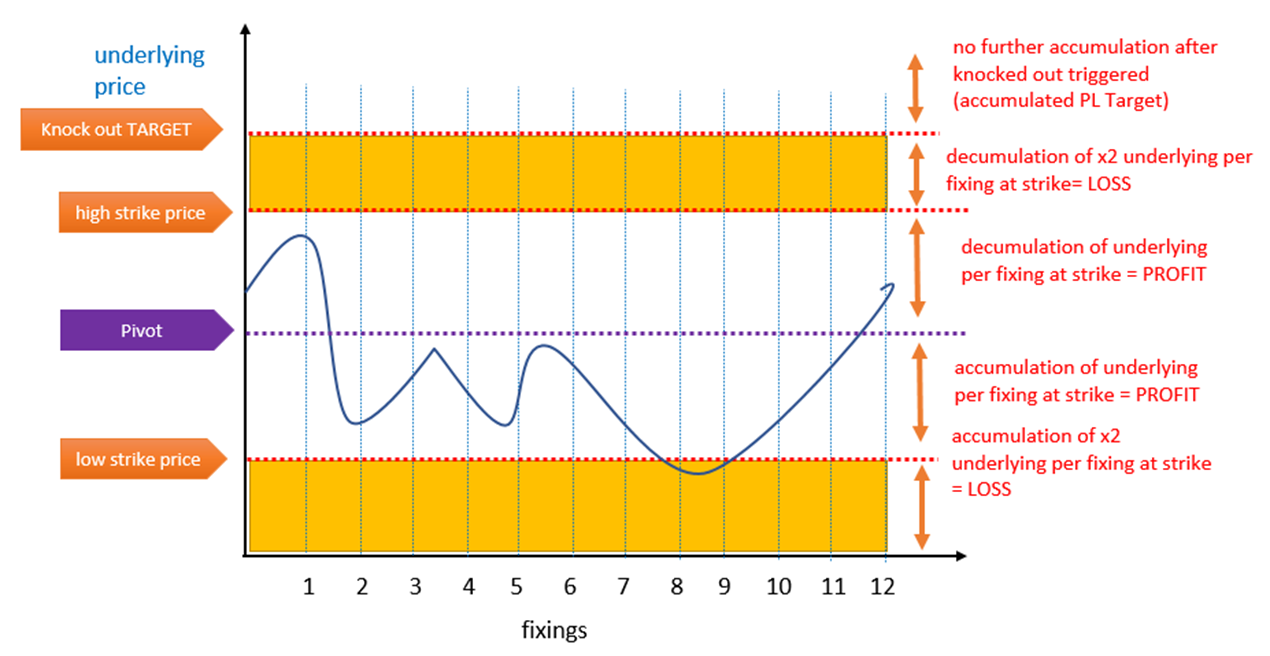

FX TARGET REDEMPTION FORWARD ACCUMULATOR with double gear & Kick In barrier

Some Target contracts may also include a kick in barrier (EKI= European Kick-in) which determines whether, if spot price exceeds strike price, accumulations are triggered or not for each fixing periods. This feature reduces potentially the client loss.

Scenarios:

1 fixing spot price > strike => investor is cumulating a profit

2 fixing spot price < strike => investor is cumulating a loss, potentially by buying x2 underlying nominal, and providing the KI barrier is reached

3 cumulated P&L >= Target => contract terminates when target is reached

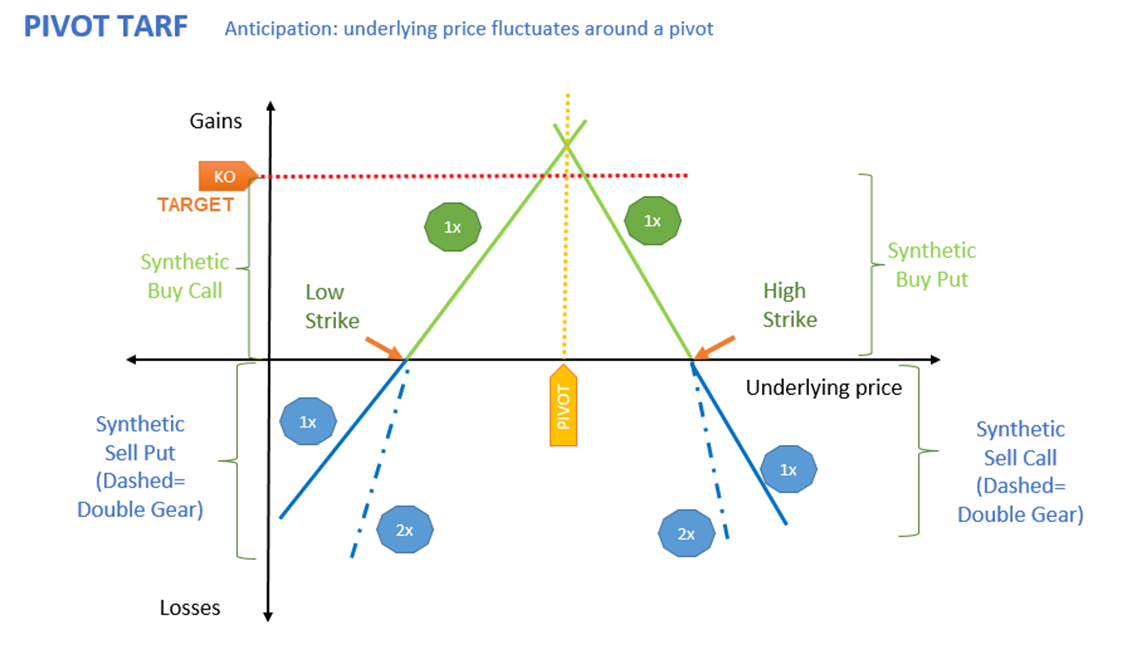

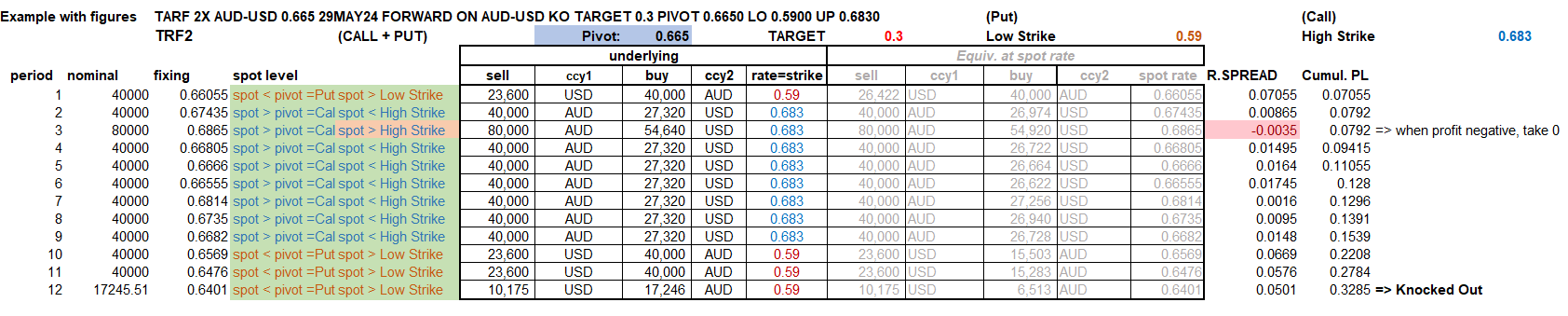

FX PIVOT TARGET REDEMPTION FORWARD (with double gear)

An FX pivot is actually a combination of a TARF accumulator and TARF decumulator.

-> If the spot rate at the fixing period is below the pivot rate: the Pivot Accumulator will be settled as an Accumulator.

-> If the spot rate at the fixing period is at or above the pivot rate: the Pivot Accumulator will be settled as a Decumulator.

The currency and the amount to be purchased or sold by the investor on each settlement date will depend on the spot rate at the fixing period. The contract terminates early [i.e. knocks out] when the cumulated P&L is reaching a pre-determined level, namely the “Target”. Some pivot contracts include a gear condition (multiplier), under which investors have to sell a certain multiples (e.g. 2x) of the stated number of the underlying when the spot price falls below/above the strike price

Scenarios:

1 fixing spot price < pivot investor is cumulating underlying (accumulator)

1a fixing spot price > low strike investor is cumulating a profit

1b fixing spot price < low strike investor is cumulating a loss, potentially by buying x2 underlying nominal

2 fixing spot price > pivot investor is decumulating underlying (decumulator)

2a fixing spot price < high strike investor is cumulating a profit

2b fixing spot price > high strike investor is cumulating a loss, potentially by buying x2 underlying nominal

3 cumulated P&L >= Target contract terminates when target is reached

Scenarios Diagram:

P&L Diagram:

FX PIVOT TARGET REDEMPTION FORWARD (with double gear) + Kick In barrier

Some Pivot Target contracts may also include a kick in barrier (EKI) which determines wether, if spot price exceeds strike price, accumulations are triggered or not for each fixing periods.